Considered as one of TRAIN Law’s most intriguing provisions ever since its effectivity was the 8% income tax rate option.

Not only did it became one of TRAIN’s most talked about rules as mentioned by most individuals, but even businesses were also interested about any developments regarding this new tax rate..

So, let’s cut to the chase: What’s with this 8% income tax rate option that makes it so special amongst taxpayers? and what are the guidelines set by the Bureau of Internal Revenue (BIR) regarding this filing option?

About the 8% Income Tax Rate

This filing option is available for self employed individuals whose gross sales/receipts and other non-operating income for the year does not exceed the three million peso (3,000,000 PHP) Value Added Tax (VAT) threshold, and are not subject to Percentage tax. In this case, they have the option to avail any of the following:

a.) Use graduated income tax rates (follow the regular rates for individuals)

b.) Avail for an 8% tax on gross sales/receipts in excess of 250,000 PHP

One the best perks in availing this option is that once you availed the 8% tax rate, you don’t need to settle for a separate Percentage and Income Tax Return. Another thing is that with the 8% option, all you need is to do is add your gross sales/receipts minus the non-taxable 250,000 PHP, then multiply the difference with the 8% tax rate and that’s it! — Simply put, this tax option would make things easier for you.

Formula:

Total Gross Sales/Receipts – P250,000 X 8%

Criteria for Availing this Option

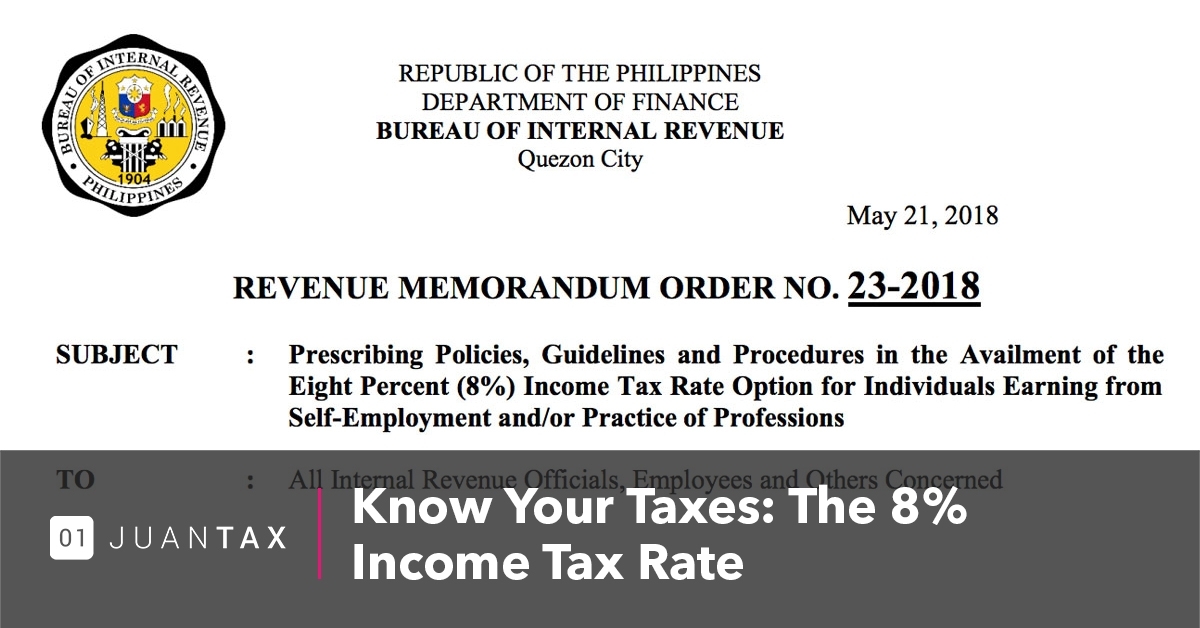

According to Revenue Memorandum Order No. 23-2018, aside from gross sales/receipts and non-taxable income not exceeding the VAT threshold (3 million PHP), here are other criteria that you should follow:

- The individual taxpayer should either be a self-employed (single proprietor, professional, or mixed income earner).

- The taxpayer shall be registered and subject to percentage tax (or non-VAT filer).

- Taxpayer should have expressed his/her intention of availing the 8% Income Tax Rate.

While those who are not qualified are the following:

- Corporation owning a business

- Compensation income earners

- VAT registered taxpayers (depending on the amount of gross sales/receipts)

- Taxpayers exempted from VAT, but exceeded the 3 million peso VAT threshold

- Taxpayers subject to other forms of Income Taxes

- Partners of GPP (General Professional Partnership).

How to File

Here are some guidelines for those who wanted to apply for an 8% Income Tax rate option:

a. For New Taxpayers

- You need to file 1901 (Application for Registration for Self-Employed and Mixed Income Individuals, Estates/Trusts.) and/or 1701Q (Quarterly Income Tax Return).

- For the initial quarter of the taxable year, you can use forms 2551Q (Quarterly Percentage Tax Return) and/or 1701Q form.

b. For Existing Taxpayers

- File BIR Form 1905 (Application for Registration Information Update).

- First Quarterly Percentage Tax Return and/or Quarterly Income Tax Return

How Juan Can Help?

For your 1701Q and 2551Q needs, you can use Juan accounting software that seamlessly integrates with JuanTax to simplify your financial data and tax compliance needs.

Juan is the Philippine’s first accounting software that is fully integrated with JuanTax, a Philippine-based cloud tax software which helps businesses in achieving compliance with the Bureau of Internal Revenue (BIR) when it comes to transactional taxes including VAT, Percentage Tax, and Expanded Withholding Tax.